Articles

Going for the Gold

08.27.2021

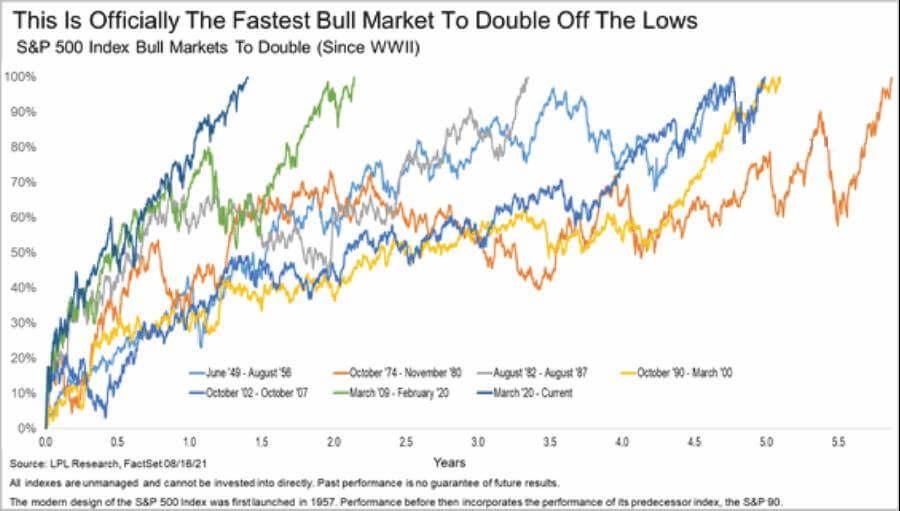

Life has been rather busy for my family this Summer, and I completely missed one of my favorite sporting events, the 100-meter dash at the Olympics. But now that Usain Bolt has retired, the event has lost a little luster, in my opinion. I can only imagine how much all of his gold medals weigh. This week the S&P 500 crossed the finish line as the fastest bull market to double off the lows surpassing the former record holder by almost a year. The current bull market took only a year and a half to double from the bottom on March 23, 2020. The previous bull market that arose from the ashes of the Great Financial Crisis now holds the silver medal taking only a little over two years to double from the lows. It should come as no surprise that this bull market that we are experiencing has rallied back so fast. Unlike previous downturns in the economy, the Federal Reserve and Congress’s power was on full display. The Federal Reserve enacted monetary policies not seen in over a decade and added new policies that helped keep struggling company’s bond prices from collapsing as entire industries shut down during the initial panic.

The Federal Government has been no slouch either, directly giving Americans thousands of extra dollars per household in stimulus and giving generous additional unemployment benefits, and issuing moratoriums on paying rent. While we can always debate the policies, and we haven’t yet seen the long-term effects as officials attempt to start winding down some of the more controversial policies, few can argue that the impact on the market hasn’t been sufficient.

So the natural question that always comes from seeing charts is when it will turn around and reverse?

I’m always curious when I get asked these questions, and I usually get the person asking to tell me what they see in their industry or daily life to shape that opinion. So I have as many conversations as possible to get a broad idea of what the market sees. Many think the recovery is just getting started and are more optimistic now than ever since the pandemic began. They point to the increasing vaccination rates and industries opening up as potential catalysts for the next leg higher in growth. On the other side, many are concerned about government spending and the inflation they see in everyday items and have keenly noted that wages are starting to rise. They are looking at a potential for companies to still make money, but that corporate profit margins will contract and hurt the earnings power of companies.

I have made some observations after having these conversations for a couple of dozen people over the last year. Older folks who lived through the 1970s are more worried about a repeat of that timeframe than people around my age. The younger cohort tends to be far more optimistic than the older group.

So who is right and who is wrong?

We will end up finding out at some point; it could be next week or next year. I think both sides make compelling points, and I have some strong opinions about what will happen, but these opinions don’t influence how we manage client portfolios over the coming months and years. As I like to tell people, predictions are often wrong but never in doubt. It’s impossible to account for the billions of variables and the billions more that will exist in the future. I would love to meet the person that predicted in 2018 what the world would look like today. If anyone knows them, please direct them my way. I would love to get their favorite numbers for the next Powerball drawing.

When we create portfolios for financial plans, we take a measured approach in estimating returns. We look at industry-leading research from several sources to develop the best estimate, always trying to err on the conservative side. The assumptions are reviewed annually, and adjustments are made systematically, much like portfolio changes. This process ensures that our estimates are driven by data and not by emotions or how we feel markets could perform in the future. In the last few years, our assumptions for both stock and bond returns have been trending lower. At some point, when the market has a sustained, sizable correction, those will start to move higher again. When assessing the probability of a financial plan’s success, 10,000 lifetimes of returns are simulated. We simulate great markets, terrible markets, and everything in between to determine the probability of success.

While the markets have put in a gold medal performance since the lows in March 2020, at some point, we may experience a sustained period where markets underperform. When a correction unfolds, investors with a long-term plan in place can be at peace knowing these types of scenarios and many others have been accounted for in calculating the long-term success of their plan. So sit back and enjoy the show.

Nathan Smith is the Portfolio Manager with Rather & Kittrell.