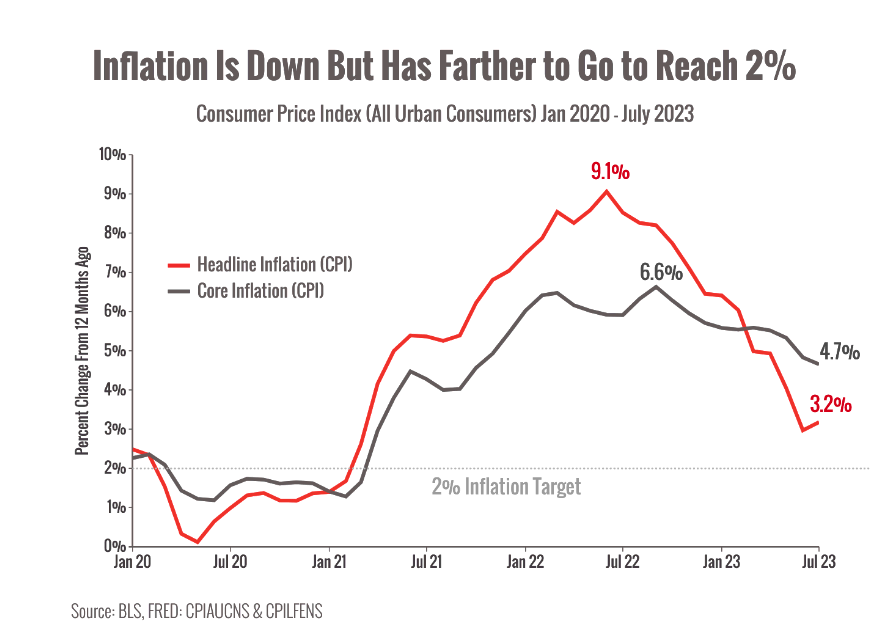

| From its 2022 peak, headline inflation has plummeted to 3.2% in July after rising slightly over June’s reading.1

Core inflation clocked in higher at 4.7% but is still well below its 2022 high.

Here’s some not-great news: Now comes the challenge of taming the last bit of inflation to reach the Fed’s target of 2%.

If you’re a fan of the Pareto Principle (often called the 80/20 rule), you might wonder if passing the homestretch will take outsized effort from policymakers.

With mortgage rates hitting historic highs and Americans carrying over $1 trillion in credit card balances, the Fed’s next moves will have big implications for consumers and the economy.2,3

What are the Fed’s options?

On the surface, the Fed has two basic options.4

Option 1: They could raise rates aggressively again to try to get to 2% inflation quickly.

That policy risks an economic downturn that the Fed is hoping to avoid to achieve their “soft landing.”

Option 2: The Fed could play a waiting game and raise or lower rates opportunistically as needed.

The risk here is that they miss their opportunity, high inflation lingers, and the Fed is forced into harsher measures that trigger a bigger downturn later.

The Fed is trying to thread the needle between just enough pressure but not too much.

Some analysts think we’re already in a “rolling recession” so the Fed may not be able to entirely avoid a downturn whichever path they choose.5

There may also be a third option but it could have even more drawbacks than the other two.

Option 3: Move the goalposts and consider 3% inflation the official new target.

Supporters say that since 2% inflation is an arbitrary goal anyway, 3% would allow the Fed more room to manage interest rate policy without damaging the current economy.

However, changing the target could cause more problems by undercutting the Fed’s credibility and signaling that the central bank no longer has control over inflation.

Since much of the Fed’s ability to do its job relies on people trusting what it says and does, losing credibility isn’t just an ego blow—it could be a big deal for the U.S.

It’ll be a tricky play whatever policymakers decide.

Let’s be prepared for more market wobbles in the weeks to come, and remember that below the surface of any short term movements in markets lies the long-term portfolio allocation that provides the foundation to endure and help achieve financial goals.

To learn more, contact us at Rather & Kittrell.

Sources:

1. https://www.cnn.com/2023/08/10/economy/cpi-inflation-july/index.html

2. https://www.cnn.com/2023/08/17/homes/mortgage-rates-august-17/index.html

3. https://www.cnn.com/2023/08/08/economy/us-household-credit-card-debt/index.html

4. https://www.wsj.com/economy/central-banking/how-hard-should-the-fed-squeeze-to-reach-2-inflation-77dbf56f?mod=hp_lead_pos1

5. https://www.msn.com/en-us/money/markets/the-recession-may-already-be-here-we-just-aren-t-calling-it-one/ar-AA1eJAkt |