Articles

Taking Stock of Bonds

04.23.2021

As equity markets reached new records for weeks on end, and the investment community was all aflutter talking about the NFT mania, GameStop, and cryptocurrency, bonds quietly had their worst quarter since 1981. The Barclays Aggregate Bond Index was down 3.4% for the quarter. The performance shouldn’t be all that surprising to investors, as yields have risen steadily since the panic lows of last March, which saw the 10-year Treasury bond trade down to an all-time low yield of .62%. I love my family, but even I would need more interest to loan my dog money than what investors were charging the U.S. government last year. Investors weren’t thrilled about the low rates, but as seen in previous sharp downturns in the market, investors sought the relative safety of bonds versus stocks. As investors began to factor in a recovery in the economy, money that had been in bonds slowly began to find its way back into the stock market. Interest rates

accelerated their move higher in February and March as the vaccination rates increased and businesses started running at a higher capacity. While the Federal Reserve has promised to keep interest rates low and liquidity programs well funded, the market thinks that interest rates may need to rise sooner rather than later. Ultimately, that is a good thing for the economy, as more people see growth ahead of us and would instead invest in stocks versus bonds in that environment.

For bondholders, it means that principal values will see pressure as rates rise, but should they be worried about a bond market “crash”?

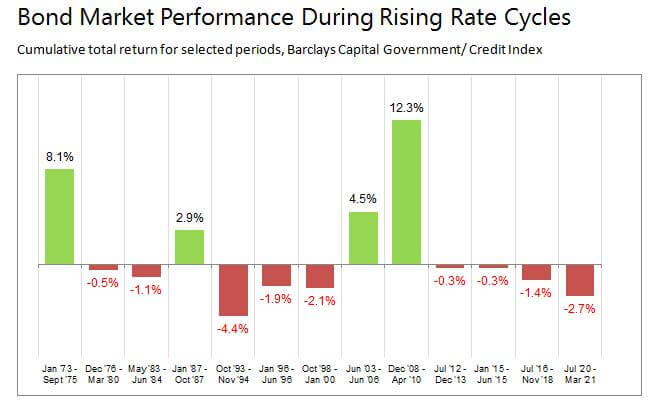

While market punditry would have you believe that rising rates are a disaster for bondholders, the data to back up that claim isn’t there. In fact, in the last five decades, where there have been 13 episodes of rising rates, bond returns during four of those periods were positive, while the others showed only modestly negative returns. The current episode that we see is one of the larger return periods, but that doesn’t necessarily mean that it will stay like that as rates continue to rise. Bonds can have down years, but stocks can perform much worse and for more extended periods.

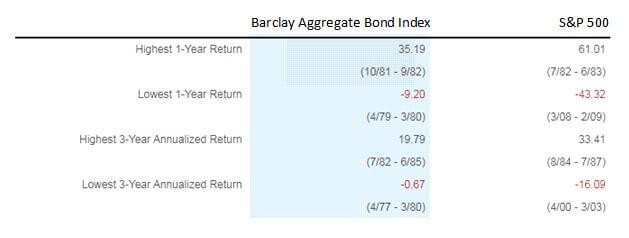

This table shows why bonds are an essential component of a truly diversified portfolio. The worst performing year for bonds was 1979, with the bond market losing 9.20%. That year the Federal Reserve decided to crush the persistent inflation through the mid to late ’70s. The actions taken by the Federal Reserve were highly aggressive and not something that the market had foreseen. The worst three-year period for bonds was an annualized performance of -.67% during the late ’70s.

Contrast this with how stocks performed during their worst one and three-year periods, and the picture becomes more evident. We all remember how stocks performed during the financial crisis, and many of us remember how the market performed in the aftermath of the tech bubble. The lowest one-year return in stocks is about five times higher than bonds, and the lowest three-year return is closer to 24 times higher than bonds.

So, while bonds may lose value during unexpected rising interest rates, they are still significantly less risky than stocks. Often, bonds are positive when stocks are down (i.e., Q1 2020), providing investors with an opportunity to rebalance. Bonds today are as critical as ever in ensuring a well-diversified portfolio that mitigates overall portfolio risk and keeps investors well anchored to their long-term financial goals.

Nathan Smith is a Portfolio Manager with Rather & Kittrell.