Articles

Should I Invest in Dividend-Paying Stocks

11.19.2021

Human beings are fascinating creatures and can be motivated to do just about anything we set our minds to, provided that the right incentives are employed. Often the motivation comes in a payout, whether it is a raise at your job or a bonus for meeting a sales goal. For example, to incentivize my Cub Scout pack to sell more popcorn, I sweetened the deal above the prizes they earn. I told them the highest-selling scout in each den or grade level would have the opportunity to hit me in the face with a pie.

I had a feeling that this would be an effective way to generate excitement and get the kids motivated to sell, and I was more right than I could have ever imagined. The Pack sold more popcorn per kid than we had in many years, and everyone thoroughly enjoyed watching their leader get creamed with pies. Listening to the kids laughing and yelling was well worth the three showers it took to get all the whip cream out of my hair.

Every day, financial markets offer investors incentives with thousands of different entities hoping to entice would-be investors to purchase their stocks or bonds. The inverse works as well, as they are also trying to keep people from selling their stock and driving their stock or bond prices lower. Companies aren’t the only entity in the market vying for capital. Governments, municipalities, and agencies are competing for investment dollars to flow into their bonds, as they incentivize investors by allowing the interest earned to be done tax-free. Some companies offer investors dividends, while others pay no dividends but offer investors the potential for higher growth rates in their share price.

Many investors prefer to own stocks that pay dividends versus stocks that don’t, and they will often search for companies paying the highest rate of dividends rather than a broad basket of companies whose combined dividends may be much lower. Banks, utilities, and telecom are usually the companies that people think about most often when these types of discussions come up.

But in an environment where interest rates are close to zero, is investing in dividend-paying stocks the right strategy for investors?

When interest rates were much higher, many investors could clip coupons from bonds or invest in dividend stocks and never touch the principal. But today, without higher interest rates, it makes it nearly impossible to achieve this strategy without dipping into the principal. The current dividend yield of the S&P 500 sits around 1.28%, which is at multi-decade lows.

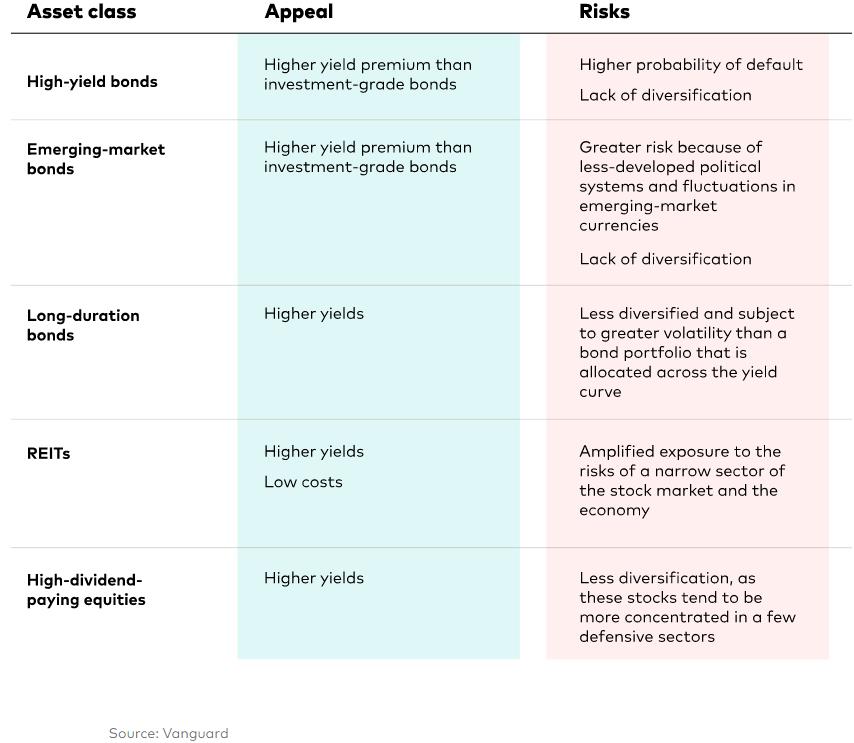

While there are companies paying higher than average dividends, investors must keep in mind that the companies are paying high dividends for a reason. Sometimes those dividends can disappear when times get tough in the economy. For example, bank stocks were paying great dividends before 2008, but many eliminated dividends or only paid 1 cent per share in the aftermath. The table below highlights some of the opportunities and risks that are present in higher-yielding alternatives.

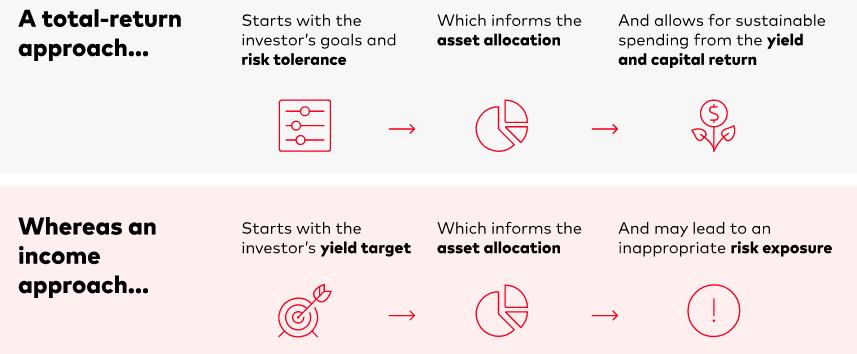

When investors target a specific yield, they may be opening themselves up to more risk than they can afford to take. The two different approaches are called “total-return investing” and “income investing.” Both try to solve the same problem but go about doing it differently. As an illustration, it looks like the following:

We favor the approach that looks at our clients’ “Why” and builds an allocation that will reach their long-term goals without taking an undue amount of risk. Allocations will utilize both dividend-paying stocks and companies focused on earnings growth that don’t pay a dividend.

As easy as it sounds to focus on the stocks that pay the highest dividends, there is a precedent for this strategy to come unglued during times of increased economic turmoil and contraction. Having a balanced approach during ever-decreasing interest rates seems like the most prudent approach investors can take, and will help keep pies from hitting them directly in the face.

To learn more, contact us at Rather & Kittrell.