Articles

Tax-Loss Harvesting

12.02.2022

| Here at Rather & Kittrell, the end of the year is a busy time. We recently had a chili cook-off, we enjoyed a large potluck Thanksgiving meal together, and in December, we will all gather again to celebrate a Christmas dinner with our spouses joining in the fun. It is a great time to be part of this team.

We also stay busy during these weeks with year-end tax planning. One opportunity we are focusing on this year is called tax-loss harvesting. While anything that includes “loss harvesting” sounds bad in a market year like 2022, the silver lining is the potential for tax savings. So what is tax loss harvesting?

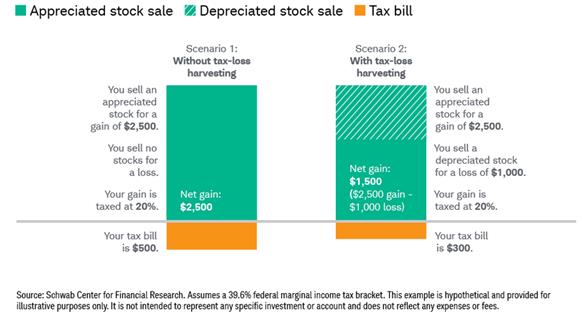

Tax-loss harvesting is the intentional process of selling an investment with a loss in a taxable account. It can be utilized only with taxable accounts, not IRA, 401(k), SEP-IRA, Roth IRA, or other retirement/tax-deferred accounts. The losses are first used to offset other gains from investment sales, known as capital gains. For example, an investor sold a position in January with a gain of $2,500. In November, the investor sold a fund with $1,000. The loss net against the gain, and this investor will only pay tax on $1,500 of gain ($2,500 – $1,000). Visually it looks like this. |

|

| In some instances, losses will be greater than any gains realized during the year and thus offset other current-year income. For example, an investor has only $5,000 of gains throughout the first part of 2022 and now has $20,000 of losses. The losses will fully negate the gains and leave $15,000 of additional losses. In 2022, the investor will reduce other taxable income by $3,000 and have $12,000 in losses to use in future tax years.

The ability to write off $3,000 of losses ($1,500 if married filing separately) is one of the few tax planning tools that reduces ordinary income (i.e., wages, IRA withdrawals, rental income, pension income, Social Security income, etc.) and is a powerful tool. While reducing a tax bill is an excellent benefit in a down year, we want to ensure that this tax-loss harvesting is also in line with our continued coaching to stay the course and stick with the plan even in down markets. Thus, when the investments are sold at a loss, we make sure to purchase another investment that is similar to the one sold and that meets the client’s investment goals. This keeps the overall mix of stocks and bonds in line with the plan AND helps with taxes. At RK, we will always help clients remain disciplined during years like 2022, and act on opportunities to couple tax savings with a well-intentioned plan. Amanda Howerton, CFP® CDFA® is a Senior Advisor with Rather & Kittrell. |