Articles

Revisiting the Behavior Gap

05.20.2022

Being a good investor is hard. Unfortunately, we have experienced an all-too-real reminder of that this year. While selecting suitable investments and keeping fees low is essential, the most important factor of investing is still the toughest to master: our behavior.

The latter half of 2020 and 2021 made investing feel easy. The market seemed to go up relentlessly without much pause. The sentiment among investors all appeared to be the same. Anything invested in the market would eventually make money, likely sooner than later. So invest what you can and stick with it. If a downturn happens, it won’t feel that bad and will probably be an excellent opportunity to invest more.

All of that sounds reasonable until you find yourself looking at red numbers on your screen or statement. Then, you feel like you have less than before, and you want it to stop.

In times like these, we risk letting emotions get the best of us by selling investments or changing the plan when the pessimism is elevated. But, historically, those moments are the absolute worst time to make a big change with your life savings.

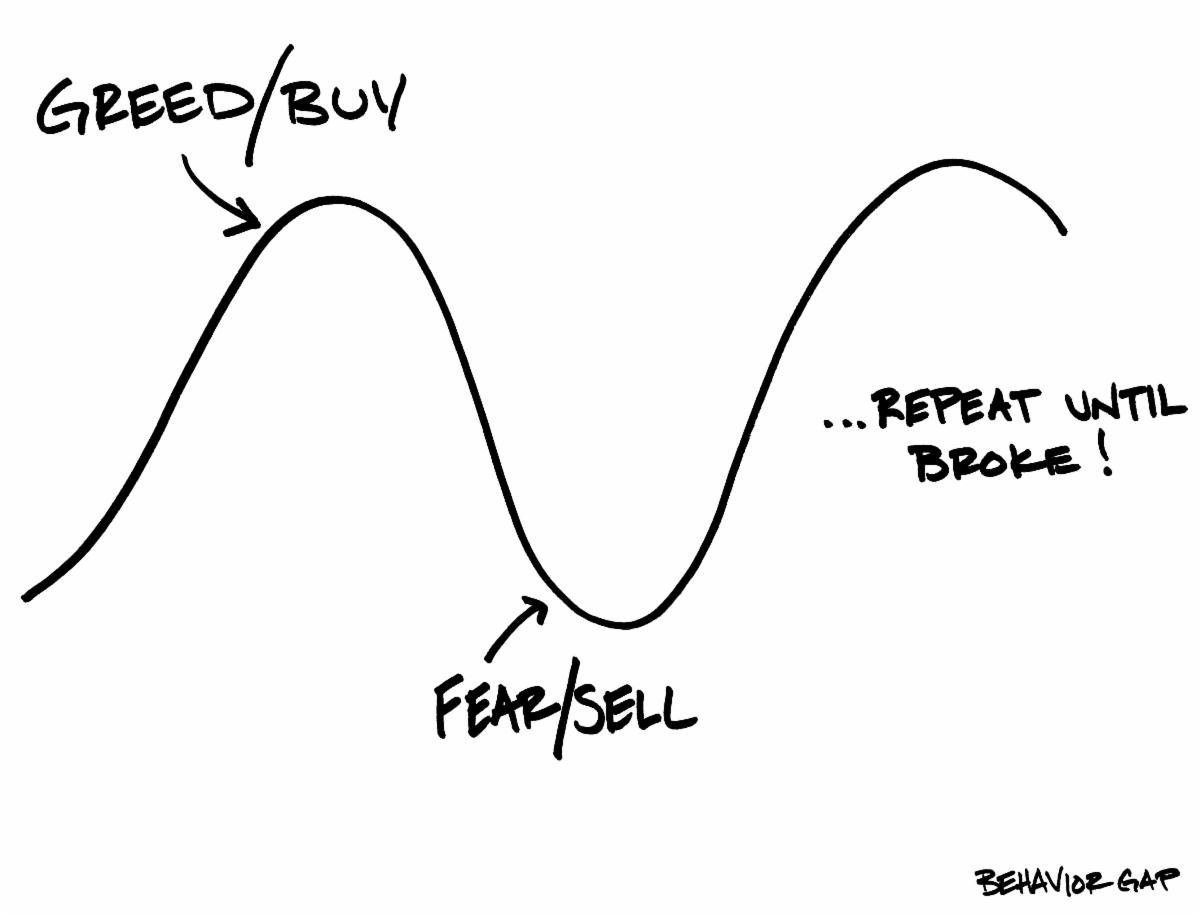

Data shows that most investors underperform the market not because of choosing bad investments or paying fees to advisors or fund companies. Instead, underperformance occurs from making mistakes when market factors cause the future to seem extraordinarily bright or bleak.

Financial author Carl Richards wrote an entire book about this phenomenon and dubbed it “The Behavior Gap.” He describes this as how investors underperform the overall markets based on poor emotional timing of investments.

The famous cliché investing advice is to “Buy when there’s blood in the streets.” The markets are far from that grisly metaphor now, but when times are difficult, that is precisely when average investors are most likely to do the opposite and cut their losses and get out of the market or at least alter their plan. These emotionally driven actions can wreak havoc on long-term investment performance.

The Behavior Gap can even show up with financial experts and their own money. For example, Bill Bengen is a retired financial advisor famous for creating the “4% Rule” of a healthy withdrawal rate in retirement. However, Bengen recently came out publicly with a revision stating that a safe spending number may need to be lower. He said the reason for this correction was that he had violated his own rule. His plan called for him to invest 50% in stocks, but his discomfort with the markets led him to shift his investment allocation to a more conservative 20% stocks, 10% bonds, and 70% cash.

Financial advisors often tell clients to stay invested and stick to a plan. Inside a spreadsheet, that is easy to do, but we live in the real world where emotions and worries about the future exist.

We can take some comfort in knowing that no down market or economy has ever been permanent, even if each new one feels like it might be the first. Having a disciplined plan and working with an impartial advisor can help us avoid falling victim to the Behavior Gap. As always, if you have any questions about your financial plan, please reach out to us. We are here to help.

Chase Kerby, CFP®, AIF® is a Senior Advisor with Rather & Kittrell.